3 days to PIT-38, no accountant. 2 hours were enough.

Today is 29 April 2026. The PIT-38 filing deadline expires tomorrow. The day before yesterday in the evening I started with a single sentence - "create a new PIT-38 project". Yesterday afternoon the return was filed with the Polish tax office, the tax was paid, and the official receipt (UPO) was sitting in output/. Total ~2 hours of active work.

5,430 transactions across two crypto exchanges. 174,895.50 PLN of unused crypto cost basis carried forward from 2024. 2 PIT-8C forms from brokers, 1 supplementary report on foreign dividends. Filed and accepted by the tax office 51.5 hours before the deadline. Final tax due: 172 PLN.

My accountant usually handles this. This year I missed the timing window - and that turned out to be one of the more instructive experiences I've had with an agentic workflow.

This article is not about how I learned to file a PIT-38. I knew what to do, because I've been doing it for years (through my accountant). It's about how two hours of active work with a properly configured agent reproduced the work of an expert service - with better documentation than I usually got from my accountant.

Quick context for non-Polish readers: PIT-38 is the Polish annual tax form for capital gains income - stocks, mutual funds, foreign dividends, and crypto. It's notoriously fiddly because of multi-source income, foreign currency conversion via central bank D-1 rates, and a multi-year cost-basis carry-forward mechanism for crypto. Filing deadline is 30 April for the previous tax year.

My accountant usually files my PIT-38

I file a PIT-38 every year. Stocks, funds, crypto, foreign dividends. Never alone. Always through my accountant - I send her the documents, she fills out the form, double-checks, files. It works.

This year I missed the timing. Deadline 30 April, and I started gathering documents on 27 April in the evening. No accountant will take a project with a 3-day buffer - and rightly so. I was forced to do it myself.

Two paths: (a) panic and a hasty last-minute filing, or (b) test whether the AI workflow I use to build things for clients can replace my accountant in two days. I picked (b). It worked.

That changes the article's stakes. This is not a "lifehack for people who don't want to hire an accountant." It's a case study of when AI automation realistically reaches into expert-level service work that until now was handled by humans.

Project architecture: every directory has one responsibility

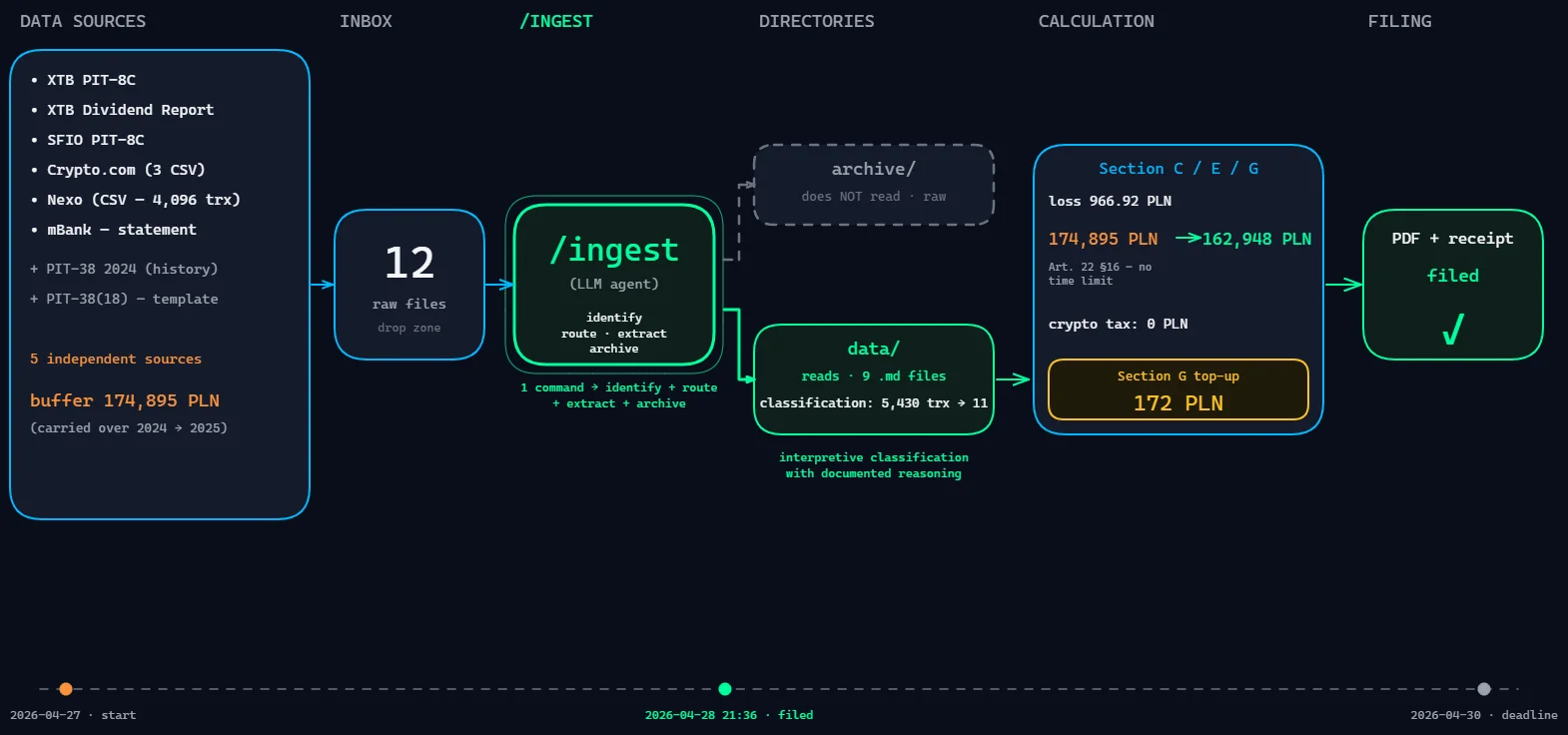

I started with the prompt "create a new PIT-38 project". No brief, no requirements doc, no task list. The agent asked about the tax year and deadline, reached for the internal _template.md convention (which it knows from the repo's CLAUDE.md), and laid out:

PIT_38/

inbox/ # drop zone, raw files

archive/ # post-processing (agent does NOT read)

data/ # knowledge - agent reads freely

deliverables/ # checklist, blog inputs

output/ # final return PDF, UPO

project.md # goal, status, decisions

catalog.md # file index

Every directory has one responsibility. The agent does not look inside archive/ or output/ unless I explicitly ask it to. This is not security - it's context hygiene. The agent works on clean, processed data/*.md files, not on 4,096 rows of raw CSV with every question.

It sounds banal. It isn't. Without that separation, every question like "what were the March transactions?" would pull the entire raw CSV into context - either blowing the token budget or forcing the model to "sum on its fingers." With separation: the agent gets a finished data/crypto-summary-2025.md with 11 line items and works on structure, not on raw input.

That's the first multiplier of value - and it works only because the convention is described in CLAUDE.md. Without that file, this project would have taken as long as doing it manually.

/ingest: one command, four steps

I dropped 7 files into inbox/: two PIT-8C forms (XTB and SFIO), three CSVs from crypto exchanges, the dividend report, and last year's filed return as historical reference. Command: /ingest PIT_38.

What happens under the hood:

- File type identification - the agent recognises a PIT-8C from its header structure, a crypto report from typical column patterns (timestamp, asset, type, amount).

- Routing - PIT-8C goes to section C of the return, crypto reports to section E, dividends to section G. Each file gets its own data/{source}-{kind}-2025.md with normalisation.

- Extraction - key items (revenue, cost, withholding tax) are pulled from PDFs, transaction types are classified from CSVs.

- Archiving - raw files move from inbox/ to archive/, catalog.md is updated, project.md gets a changelog entry.

A concrete example: PIT-8C from both XTB and SFIO ended up summed in pit38-calculation.md in section C, using line numbers consistent with the PIT-38 form version (18) for tax year 2025. The agent itself noticed that this was not the same form layout as 2024 - more on that shortly.

The lesson at this stage: /ingest is not batch processing. The value lives in the iterative loop, which I'll show next.

Six things I didn't expect from the agent

This is the heart of the article. Six concrete things the agent did across those two days that, had I worked alone with Excel, I either wouldn't have done at all or would have done with errors.

1. The 174,895.50 PLN buffer - auto-pulled from PIT-38 2024

Under Polish PIT law, unused crypto cost basis rolls forward indefinitely (Art. 22 §16 of the PIT Act). It's a standard mechanism for active crypto investors.

I knew this buffer existed - I've been filing PIT-38 for years. But I knew it from the perspective of "tell my accountant about it," not from the perspective of "enter it in field 38 of the new form precisely."

On the first ingest pass, the agent asked for last year's return. I uploaded the 2024 PIT-38 PDF. The agent itself extracted the amount from the relevant line and entered it in the matching slot of the new return - where it becomes "costs from prior years."

Value to me: that buffer is usually "remembered" by the accountant, who has my prior year's return in her CRM. Without her, I would have had to remember on my own to download the PDF, open it, find line 38. The agent did that with a single question.

This is an underappreciated class of value - automating "easily accessible memory of prior years' context." Accountants do it. Agents with access to historical files in archive/ do it.

2. PIT-38 form version (17) vs (18) - the small detail that breaks a return

In PIT-38 for 2024, prior-year crypto costs lived in one line. In 2025, that line moved. Section C in version (18) gained an extra row for exemptions under Art. 21 §1.105a - and everything below it shifted by two lines.

Many blog posts and online forums still reference the old line numbering. If I had entered the data into the old positions, the return would either be rejected outright or, worse, accepted with a calculation error that would surface during an audit.

The agent caught this after I uploaded the blank PIT-38(18) form template as reference. It compared the structure with last year's filed return, flagged the differences in data/sources.md, and used the new numbering in the final calculation.

Lesson: trust reference documents, not the model's memory. A current form template uploaded > whatever the model picked up from training data a year ago.

3. 5,430 transactions → 11 taxable events

4,096 transactions from one platform plus 1,334 from another. 5,430 raw rows in total. After classification: 11 taxable events that go on the return. The rest are platform-internal operations - transfers, technical adjustments, accruals, small reconciliations - that don't need to be reported.

The LLM's value here is not in summing. It's in classification. Each of the ~25 transaction types in the report was assigned to one of three categories: taxable event / internal operation / neutral. Each classification was backed by a documented legal rationale in data/sources.md.

I won't go into specific transaction types or legal interpretations - that's beyond the scope of this case study and requires individual consultation with a tax advisor. I'm only showing the scale of the classification work.

Without that classification, trying to file 5,430 raw CSV rows manually would have been either impossible in two days or would have led to a dramatic overstatement of the tax base - if I had treated every transaction as a disposal. The scale that the LLM reduces here is non-trivial.

4. Central bank D-1 FX rates - 10 edge cases with a holiday calendar

Every transaction in EUR/USD has to be converted to PLN using the mid-market rate from the National Bank of Poland (NBP) on the business day before the disposal date (Art. 11a of the PIT Act). Sounds simple. In practice 10 of the 11 transactions needed individual handling, because they fell on non-business days:

| Transaction date | Day of week | NBP rate from |

|---|---|---|

| 2025-02-15 | Saturday | Friday 2025-02-14 |

| 2025-03-16 | Sunday | Friday 2025-03-14 |

| 2025-05-02 | Friday | Wednesday 2025-04-30 (1 May = public holiday) |

| 2025-05-18 | Sunday | Friday 2025-05-16 |

| 2025-06-15 | Sunday | Friday 2025-06-13 |

The agent did this manually for each of the 10 transactions: computed the day of week, checked national holidays (1 May, 3 May, Corpus Christi, 15 August, 1 and 11 November, 25-26 December), pulled the rate from NBP, applied the conversion.

This is exactly the kind of work where a human brain trips up quickly - every edge case requires checking a calendar separately. A human would make 1-2 mistakes per 10 transactions (forgetting 1 May is a common Polish-tax bug). The agent made 0.

The class of task "many small mechanical decisions with subtle rules" is an LLM's strength. Not summing. Not creativity. Systematic application of rules to each of 10 situations without boredom and without omission.

5. The 6 groszy the LLM couldn't add up

My calculation for section C: a loss of 966.98 PLN. The official tax-office portal after data ingest: 966.92 PLN. A 6-grosz (0.06 PLN) discrepancy. Arithmetic error from the LLM when subtracting two 6-digit numbers (16,188.05 − 15,221.13).

Lesson: LLMs make arithmetic errors on 6-digit additions. Leave summing to a calculator, Excel, or the tax-office system. The LLM has value in structure and interpretation, not arithmetic. This isn't a failure - it's a map of where to use the tool and where not to.

In this specific case the tax-office portal corrected my error for free. In another scenario - say, a paper filing - a 6-grosz delta would have gone to the tax office and probably no one would have cared, but the principle stands: arithmetic to a compute engine, not to a language model.

6. Ingest as progressive discovery - the strongest beat

The most valuable thing the agent did across those two days was not summing 5,000 transactions. It was asking about things that weren't on my list.

I didn't have a list of "what's needed for PIT-38." I uploaded what I had at hand. After each iteration, the agent said: "OK, this is here, but X is missing" or "watch out, this implies Y, check Z."

The key moment: foreign dividends.

- I didn't know I had dividends from 2025 (small ETFs in XTB, around 958 PLN gross).

- I didn't know they have to be reported separately from everything else (section G of PIT-38, Art. 30a, 19% PL minus withholding).

- After the first ingest, the agent asked: "and what about dividends? PIT-8C doesn't include them, XTB issues a separate report."

- I downloaded the XTB Supplementary Report for PIT-38 - and there were 182 PLN of 19% PL tax on foreign dividends to declare.

Without that question, I would have filed the return without section G. Result: a 172 PLN underpayment, audit risk, late-payment interest.

The second moment: 2024 history. On the first ingest the agent asked whether I had last year's return. I uploaded the PDF - and that's when the 174,895.50 PLN buffer described above surfaced. Without that move I would have paid ~2,200 PLN in tax instead of 0.

This is the essence of the value: not "the agent summed transactions," but "the agent knew what I didn't know." Iterative questioning + classifying every document against the PIT-38 taxonomy = impossible to achieve manually without specialised tax knowledge.

Ingest workflow ≠ batch processing. The value is in the loop: you upload → the agent classifies → it identifies gaps → it asks for more → you upload again. After 3-4 iterations you have a complete picture you couldn't have assembled on your own.

A short primer: how crypto taxation works in Poland

A small explainer for readers outside Polish crypto-tax topics, so that "buffer of 174k" doesn't read as "Pawel lost 174k."

Under Polish law (Art. 17 §1.11 of the PIT Act), a taxable event arises only when crypto is exchanged for traditional currency or for goods. As long as you hold a crypto position - regardless of how the market value moves - you don't report anything. Crypto-to-crypto swaps are also neutral (Art. 17 §1f).

If you buy crypto for 100,000 PLN and don't sell for fiat for several years, that 100,000 PLN exists as a documented cost of acquisition (Art. 22 §14) and waits. In the year you sell crypto for fiat, that cost reduces the taxable base. If costs > revenue in a given year, the surplus rolls forward indefinitely (Art. 22 §16).

That's where the "buffer 174,895 PLN from 2024 → 162,948 PLN for 2026" comes from in my case. It's not a loss - it's expenditures on crypto purchases I haven't yet closed via sales to fiat. The buffer shrinks only when I actually sell crypto for PLN/EUR/USD.

This is a heavily simplified description of the mechanism. Full understanding requires consultation with a tax advisor - this is not tax advice.

Interpretive decisions: where the human comes back into play

With 5,400+ transactions across multiple platforms, some categories of events have ambiguous tax classification. There are differing opinions from the Polish National Tax Information service (KIS), differing tax-advisor positions, and administrative-court rulings touching adjacent constructions.

For each such category, the LLM laid out arguments for both sides, estimated risk exposure, and showed me the numerical trade-off - how much tax a conservative interpretation implies, how much a less restrictive one, and what the dispute risk looks like with the tax authority. I made the decision, not the agent. The agent left the rationale in data/sources.md in the repo - if an audit ever comes, I have a documented chain of reasoning.

And one more key point worth repeating to anyone facing a first solo filing: a PIT-38 amendment is possible up to 5 years back (until 2030 for the 2025 return). Filing in good faith with documented decisions = a safe path. When you're not sure, a conservative interpretation in the first filing always works - you can later amend in your favour.

In this section the LLM does not decide for me. It maps options, documents arguments, waits for input. That's exactly the division of labour I want.

"You uploaded financial data to an LLM?" - a deliberate choice, not carelessness

I know that for some readers, "I uploaded financial data to an LLM" is already disqualifying. Three things to consider.

a) Claude Code (Anthropic API) does not use data for training models by default. It's a different business model from consumer ChatGPT - and a qualitative difference. Current data-handling rules are always worth checking in the Anthropic privacy policy, but the baseline is this: the API is a production environment for developers and businesses, not a training-data harvester.

b) The repo is private and local. There is no git push to GitHub. CSV files are in .gitignore - they don't even enter commit history. Raw financial data sits only on my disk. The LLM's context ends with the conversation.

c) A real benchmark. The alternative was an accountant at a desk, an Excel file on a USB stick, or the tax-office portal in a browser - in every one of those scenarios my data passes through someone's hands, someone's memory, or someone's servers. The choice is not between "safe" and "risky." It's between different kinds of trust.

I deliberately chose to trust Anthropic + a local workflow. Someone else will choose differently and that's fine. The discussion "is an LLM safe for finances" loses meaning if we don't compare it to a concrete alternative.

What I don't recommend

- I didn't automate the 172 PLN payment. The transfer to the dedicated tax microaccount went manually. There's no point doing that through an LLM - one amount, one account number, 30 seconds in the banking app.

- I don't recommend this setup to anyone without programming comfort. /ingest, directory structure, git, .gitignore, markdown editing - it requires familiarity with the tools. Without that, the time spent on setup eats all the gains.

- An LLM does not replace a tax advisor. In ambiguous situations - and there are plenty when you have multi-source crypto + stocks + dividends - the final call has to belong to a human, ideally after a consultation with an advisor. The LLM provides arguments and maps risk. The advisor gives a recommendation tailored to your situation and takes responsibility for it.

If you're reading this today - you still have ~30 hours

If you haven't filed your PIT-38 yet and you have multi-source income, here's a minimum-viable plan for 2-3 hours before the 30 April deadline:

- Download every PIT-8C from your brokers (XTB, mBank, etc.) and reports from your crypto exchanges.

- Open the official tax portal (Twój e-PIT) - section C (stocks + funds) is auto-filled for most people.

- Sections E (crypto) and G (foreign dividends) have to be filled manually. This is where the portal won't help you.

- Check your PIT-38 from 2024. See whether the relevant line carries unused crypto costs from prior years. That can be a buffer worth a few to a few tens of thousands of PLN that you might have forgotten about.

- File via Trusted Profile (Profil Zaufany). Pay the microaccount by 30 April.

- Worst case: a PIT-38 amendment is possible until 2030. Filing a roughly correct return on time is always better than no return + late-filing waiver paperwork.

After the deadline, in three profiles:

- Simple PIT (one PIT-37 from employment) - Twój e-PIT and that's it. Don't overcomplicate.

- 2-3 sources (stocks + crypto) - worth considering an evening or two to set up a workflow like this.

- 5+ sources and a history of carried losses - this is your scenario. The crypto cost-basis buffer can be worth 5-50k PLN in overlooked tax annually. The setup pays for itself.

The value of an LLM grows not linearly but in jumps, when the repo's structures are legible to it. Without CLAUDE.md and project conventions, this project would have taken as long as working with an accountant. With them - two hours. That is exactly the ROI range that can't be sold via generic content marketing - because it requires the infrastructure to be there first.

Got multi-source taxes and thinking "I want this too"?

I help freelancers and technology consultants set up AI workflows for the kinds of work they used to delegate to experts. I'll show you what such a setup could look like for you.

Book a free consultationUseful Resources

- Twój e-PIT (Polish tax portal) - auto-fills section C for stocks and funds

- Polish PIT Act - ISAP - Art. 17 §1.11, Art. 22 §§14, 16, Art. 11a (FX rates), Art. 30a (dividends)

- NBP - average exchange rates - D-1 rates for FX transactions

- Anthropic - Privacy & Data Usage - default API data handling

- Skills 2.0 - multi-agent system for company management - context for how CLAUDE.md conventions are built

- Spec-driven SEO on portfolio and Qamera AI - another case study, same workflow class

FAQ

Can I do PIT-38 with Claude Code if I'm not a programmer?

Short answer: probably not worth it. The setup requires familiarity with git, the terminal, directory structures, markdown editing, and .gitignore. Without that, the time spent configuring eats all the gains. A safer path for non-technical users is an accountant or the official tax portal with manual entry of sections E and G.

Does Anthropic use my financial data to train models?

By default, no - Claude Code (Anthropic API) operates under a different business model than consumer ChatGPT. Data sent through the API is not used to train models without explicit customer consent. It's a different category from free consumer tools. Always worth checking the current rules in the Anthropic privacy policy.

What is the "crypto cost-basis buffer" and why can it be worth tens of thousands of PLN?

The buffer is your documented spending on crypto purchases that you haven't yet closed via sales to fiat currency. Under Polish PIT (Art. 22 §§14, 16) those costs wait in a buffer until the year you sell crypto for fiat - then they reduce the taxable base. Any surplus of costs over revenue in a given year rolls forward to subsequent years with no time limit. That's why checking last year's return can be worth several to several tens of thousands of PLN in overlooked buffer.

What if I'm reading this after 30 April and haven't filed PIT-38?

File as soon as possible with a "czynny żal" (active regret, Art. 16 of the Polish Fiscal Penal Code) - the penalty for non-filing grows with time, and czynny żal in many cases lets you avoid the fine. A PIT-38 amendment is possible up to 5 years back, so it's better to file a roughly correct return late than not at all. Afterwards, consult a tax advisor if your situation is complex.

Does an LLM replace a tax advisor for multi-source PIT?

No. An LLM is good at classifying transaction types, extracting data from PDFs, and mechanically applying NBP exchange-rate rules - but in cases of ambiguous legal classification the final call must belong to a human. Ideally - after a consultation with an advisor who takes responsibility for a recommendation tailored to your situation. The LLM maps options and risks. The advisor makes the decision and signs their name to it.